Scientists in Antarctica are playing Candy Crush Saga. Sherpas in Nepal chat on their phones while hauling 75-pound loads up mountains. Samoans are FaceTiming on the beach on 4G, and San Francisco hipsters are ordering designer coffee, custom-fit t-shirts, and massages for their pets via mobile.

What’s going on?

The mobile economy is reaching a global tipping point in 2016. Everything is changing, and the giants of industry are under attack by new startups with an app, a community, and — to the quick glance — not much else. Here are my 16 (somewhat belated) predictions for the coming year.

1) Hello, mobile majority moment

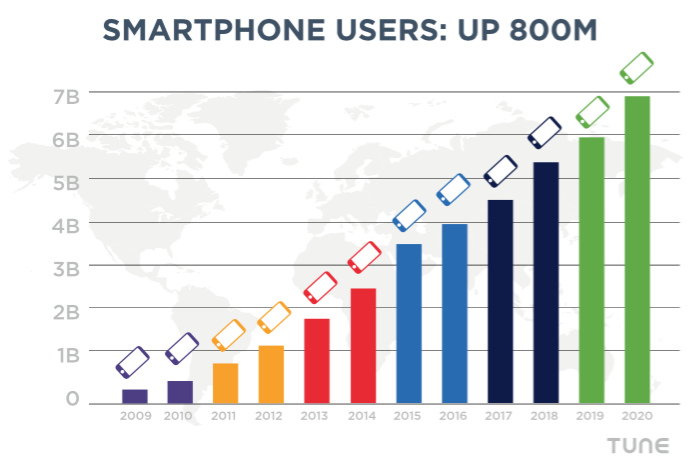

In 2016, more than half the planet will own and use a smartphone. 800 million joined the club in 2015. Another 600 million will in 2016, according to Ericsson, and that means smartphone penetration will punch through the 50% point, globally.

Global mobile users will reach almost 7B in 2020. Data from Ericsson and TUNE forecasts.

If you think for just a moment about the changes smartphones have brought to the U.S., Canada, and Europe since Steve Jobs unveiled the first iPhone in 2009, it’s clear that the social, financial, and legal ramifications of this are hard to quantify.

2) Mobile makes IoT feel real

The internet of things has been the next big thing for some years now.

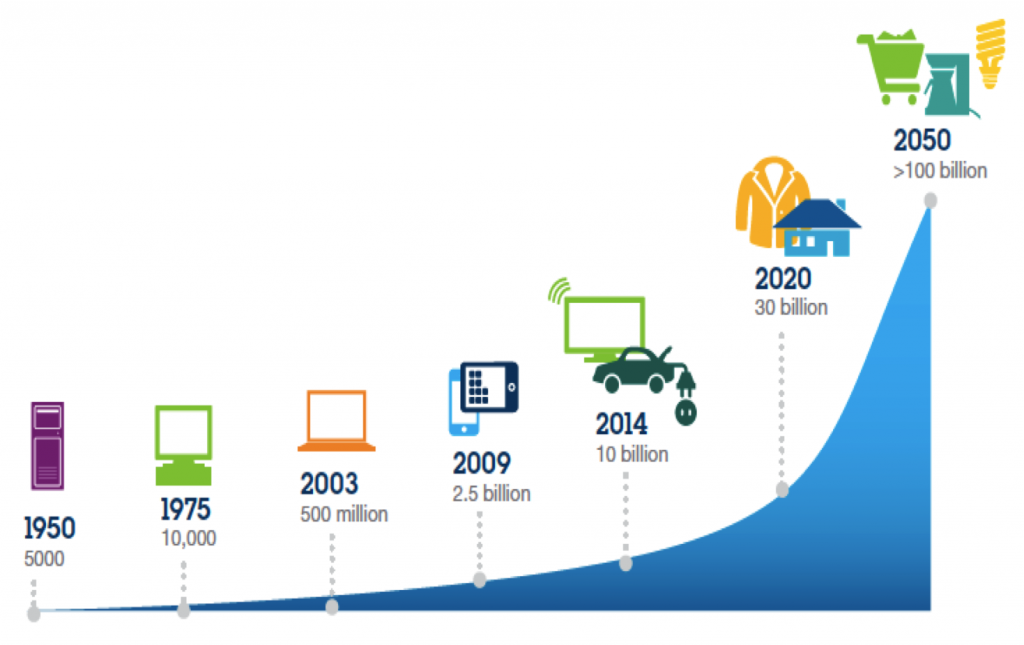

But 2015 was the year that IoT’s growth rate actually surpassed mobile’s growth rate. As more and more people around the world get smartphones, the incremental growth rate has been dropping, and is now in the low two digits … about 15-20%. IoT devices in industries, homes, and cities are growing faster than that.

Data from IBM on the growth of IoT

But, the phone is taking its place as the central controller — via apps — for our smart doors, fridges, furnaces, chairs, cars, and more. The form factor will continue to change, but what the phone currently does is aggregate access to smart things and systems for authenticated individuals, and we’re going to see that continue.

3) Smart matter for everyone

Building on the previous point, while 2015 was the convergence year when IoT growth rates exceeded smartphones, 2016 will be the year the vast majority of non-early adopters will have their initial experiences with smart matter.

Smart matter is the stuff of IoT: things with sensors, things with network connectivity, things that communicate, and things that adapt and respond intelligently to circumstances or commands.

4) The quad screen battle will intensify

Glu CEO Niccolo de Masi has talked about the quad-screen future: phone, tablet, TV, and laptop. While we’re rapidly approaching a point at which some of those distinctions matter less and less, there’s still a definite difference in how we choose to do work, do social, do entertainment, and other things.

Google’s Chromecast

Bigger screens enable not necessarily better but different experiences; similarly, smaller screens enable not better but different opportunities. And, it’s not one-size-fits-all … what works for you may not work for tweens or gen-Yers.

In 2016, we’ll see companies like Apple, Google, Microsoft, Amazon, and Samsung intensify their battle to own a single customer relationship with one billing set-up, shared content, a consistent user experience, and common app availability across phone, tablet, TV, and, to some extent, laptop.

5) App integration becomes inevitable

The web allows quick and easy integrations, at a low level, via simple links. And higher-level integrations, albeit slower, via APIs. Native mobile apps, which started out as small bits of code living relatively siloed lives on small pocketable devices, evolved the opposite way: higher-level integrations via SDKs came first, and only relatively recently, deeplinking.

The famous Uber-Spotify partnership

In 2016, app integrations will explode.

Why wouldn’t you add a delivery service link to your m-commerce app, so people can get their product in hours or days? Why wouldn’t you add a reservation service to your tourist app, so users can immediately act on impulses?

The web is subdivided by tabs in browsers, and mobile has been subdivided by insulated app experiences, but this is changing.

6) App store optimization will change forever

ASO may seem to be the new SEO, but it has been a vastly less mature space. Where Google and others have iterated on web search to find not only the meaning and significance of content on the web — to the extent of currently beginning to understand queries, understand facts about the world, then understand and formulate answers from websites — app store optimization has primarily been about meta-data, not data.

In other words, your app’s rankings have primarily depended on keywords, name, description, download velocity, ratings, and reviews … all of which have been taken by Google and Apple as indicators about the content, capabilities, and experience inside your app.

That’s about to change, as both major mobile platforms start to look deeper, see the content inside apps, index it, and make it available not only inside the app store but also in web search (Google) and Spotlight search (Apple’s on-device universal search capability).

7) Android vs iOS is over

In 2014 and to a large extent still in 2015, you could identify differences between iOS and Android users and potentially make sense. Today, and increasingly in 2016, that’s no longer the case

In the dim mists of mobile antiquity, iOS users were rich and Android users were poor. That might still seem the case — particularly in China, see our recent report — but if you look closer, the real difference is between high-end devices and low-end devices.

Cheap Android smartphones

Do you really think the HTC One A9 ($500) buyer is the same as a generic Android burner phone ($37) buyer? Not in the least. And they can’t be treated that way.

8) Asia, Asia, Asia

The amount of growth in Asia is incredible. Two of the most populous countries in the world — and fastest developing — are in Asia. Many of the other fastest-growing companies are in Asia as well.

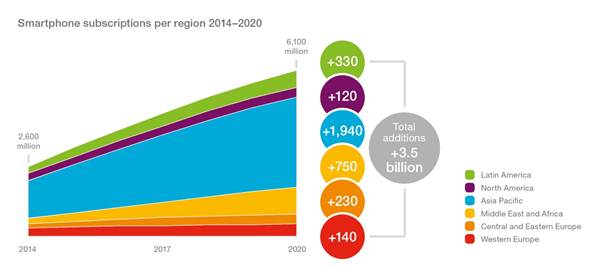

Ericsson data on where new smartphone subscriptions will come from

Almost 80% of new smartphone subscriptions to 2020 will come from Asia, according to Ericsson. At TUNE, we’ve seen the same thing — and BRIC countries Russia and Brazil will push that number even higher. BRIC already comprises a large part of our business, and it doubled in 2015.

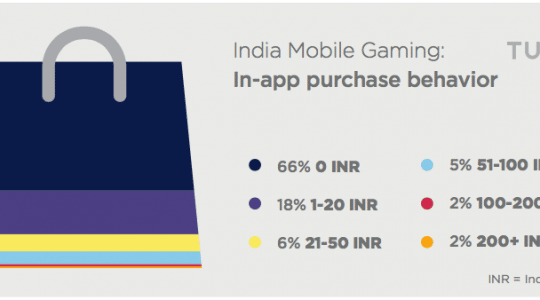

In 2016, expect more from Asia. Expect reverse technological colonization. Mobile and web giants of Asia such as Alibaba have already looked West for increased profits. Tencent has invested in the U.S. Korea has wealth and know-how. India is mobile-first and can teach old-fashioned westerners a thing or two. Japan still has gaming and technological chops.

Expect some of that mobile savvy and the financial rewards that came with it migrate west and take up leadership positions in key categories.

9) Messaging mania rages on

It’s obvious that messaging is hot.

Communication, messaging, and social apps dominate the top 20 list, with names like Facebook Messenger, WhatsApp, Snapchat, LINE, and WeChat. Plenty of other messaging apps have significant and in some cases even global size and scale: Viber, Kik, Skype, if you want to put it in this category, QQ Mobile, and more. Why?

Everyone wants what WeChat has created in China: a mobile connection, commerce, and payments ecosystem powered by conversation and messaging. Facebook will try to replicate parts of this in Messenger. Tiny startups like Cola are trying to reinvent messaging with context and intelligence.

The real question is how Apple (iMessage) and Google (which has a variety of SMS apps) will respond.

The clear direction, however, is to an increased emphasis on messaging as a platform, and perhaps even a new kind of operating system for commerce and communication.

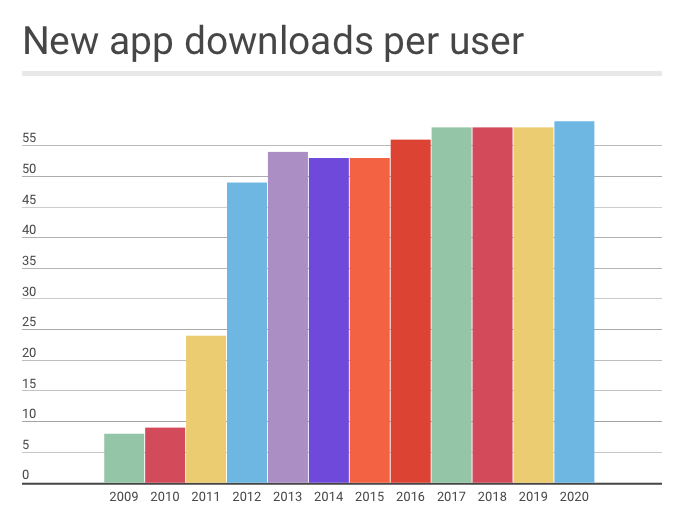

10) App download rates stagnate (sort of)

If you’ve been paying attention, app download rates are stagnating. We saw this first 18 months ago, when comScore revealed that a significant majority of American adults — 65.5% — don’t download any new apps in any given month.

Along with other factors, this is the result of an extreme power law in mobile: winners win like they’ve never won before.

New app downloads to users: not increasing fast

People use maybe 20-30 apps in a month, and the vast majority of that is in only 5-8 apps. Everyone’s 20-30 is a little different, and their 5-8 vary slightly as well, but all told, about 200 apps account for the vast majority of our total mobile time. All of which means: we have limited time to even think about wanting other apps.

But, there are a few caveats to this trend. First, while few adults are looking for new apps, tweens and teens and millennials often are. Second, as trend #3 (Smart Matter) takes hold, more and more products that formerly were dumb (in both the old-fashioned sense and in the newer-fashioned sense) and deaf are neither. And the language they have been taught to speak is app… we will control them via apps.

So I, for example, now have a Home folder for apps, where WeMo, Nest, and Tile live, and many more will join them.

And third, as new platforms take hold — think Apple TV, other smart TV systems — there are new opportunities for apps and brands to stake their claims.

11) Engagement is the new user acquisition

User acquisition has driven billions of dollars into the mobile advertising ecosystem as Supercell and King and Kabam and EA have aggressively expanded their player communities, and as social apps and messaging apps and ride-sharing apps similarly have seen user acquisition as the first logical step in customer acquisition.

But everyone in mobile knows that download numbers are meaningless. Engagement matters. Time in app matters. Events in app matter. Social mentions matter. Ultimately revenue matters. And you don’t get revenue without engagement, which is one of the reasons TUNE added in-app marketing, also known as mobile marketing automation, to our suite of products.

12) User acquisition costs will jump (again)

This one’s not rocket science.

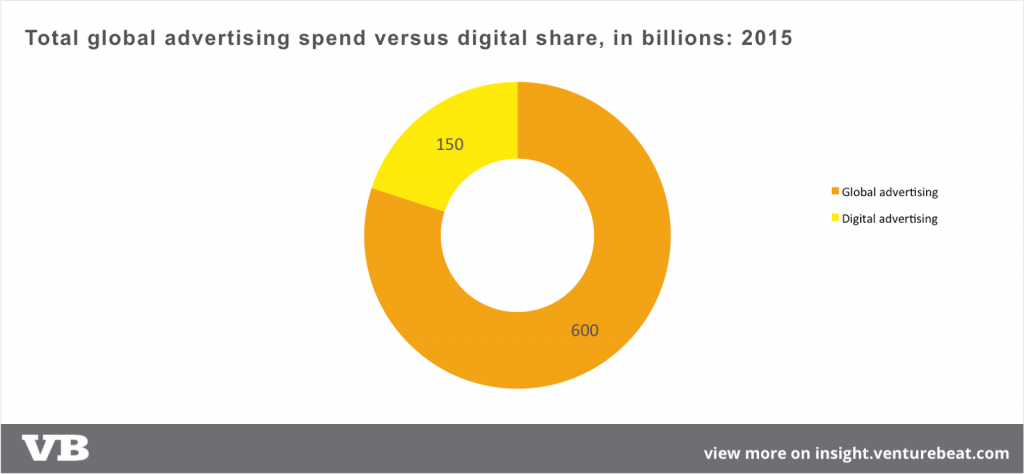

Last year, mobile advertising hit $51 billion in the U.S. By 2020, that number will be $105 billion, according to eMarketer. But we’re already spending more time in apps than on TV, which sucked up disproportionately more ad dollars — $71 billion — in 2015. Globally, the picture is similar:

Global ad spend, via VentureBeat

So there’s more money coming. The vast majority of the global $600 billion ad spend is coming to mobile over the next few years. Mobile is growing too fast to ignore, as is video on mobile, and ad dollars naturally follow people’s attention. The result? Demand growth will outpace supply growth. And the inevitable result of that: rising prices.

All of which, of course, makes #11 (Engagement is the new User Acquisition) even more critical.

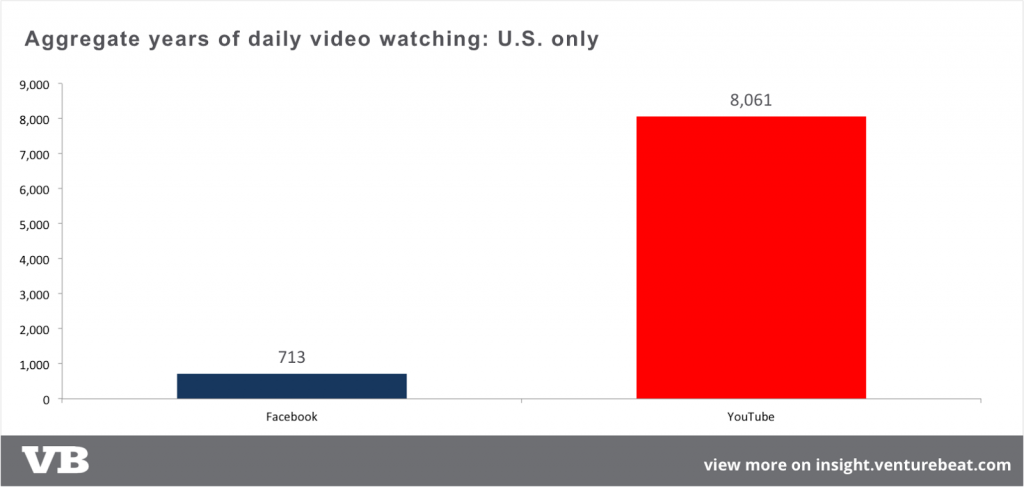

13) Mobile video: Facebook fights YouTube head on

Facebook’s video growth is massive, seemingly doubling every quarter. While it’s still second fiddle to Google’s — err, Alphabet’s — YouTube in terms of minutes of engagement, it doesn’t take too many periods of doubling to erase a lead.

Facebook vs Google: video time circa September 2015

But Facebook has some challenges.

First, time spent in videos for Facebook versus Google: while people watch YouTube for hours, they pop out of Facebook videos in seconds or minutes. Second, Facebook counts views at three seconds, which is a little aggressive, perhaps. And third, Facebook doesn’t really have something analogous to YouTube’s creator class, who make significant amounts of cash off and ad-split on their video channels.

But Facebook’s momentum is virtually unstoppable. And with Oculus Rift, 360-degree video, and potentially a video-consumption-centric app in addition to its video-consumption features … Facebook will challenge YouTube even more.

14) All those remotes will go

How many remote controls live in your home, on your shelves, and in the creases and folds of your sofa? Too many.

When every device can have WiFi, this is insane. The phone is not only making IoT feel real, it is becoming the remote control for your life. This is obvious when you see what companies like Sonos and Bose are doing with their products, and TV manufacturers will succumb at some point.

Sonos on your iPad

(Especially, and perhaps worrisomely so, because it could tie into usage tracking and actual relationship — imagine that — with your TV or stereo manufacturer.)

15) Health goes big data, thanks to mobile

All the big studies on health and food and activity from the 1960s to 2010 will soon be historical oddities, barely trusted, if at all, by medical professionals. Google Fit and Apples HealthKit, along with ResearchKit, are enabling both much broader sampling and much more reliable data.

And while scientists can argue over whether Fitbits provide medical-level research-grade data, which would you trust: people’s own noted recollections of what they might or might not have done, or an instrument that continually measures what they actually do, in real time?

In 2016, we’ll start to see health studies using mobile and wearable-generated data become more trusted than conventional studies, thanks to the NIH and many others.

16) Beacons continue to squawk, but still fail

(I owe this one to TUNE CEO Peter Hamilton.)

Various beacon devices

Beacons will continue to be solutions in search of a problem. We’ll continue to hear about cool technology and cool capabilities and cool use cases, and we’ll continue to almost without exception fail to experience them personally, in the real world, in any meaningful way.

Author

Before acting as a mobile economist for TUNE, John built the VB Insight research team at VentureBeat and managed teams creating software for partners like Intel and Disney. In addition, he led technical teams, built social sites and mobile apps, and consulted on mobile, social, and IoT. In 2014, he was named to Folio's top 100 of the media industry's "most innovative entrepreneurs and market shaker-uppers." John lives in British Columbia, Canada with his family, where he coaches baseball and hockey, though not at the same time.